Helicopter Hope

Note: I first published this Opinion Piece on November 2, 2016. A version of this was adapted for MarketWatch (link provided below). The charts were updated on September 1, 2017. -- Minyoung Sohn, CFA.

Chairman Alan Greenspan talks to Sara Eisen of CNBC on October 6, 2016. In this interview with CNBC's Sara Eisen, Former Federal Reserve Board Chairman Alan Greenspan discussed the risk of stagflation and unequivocally expressed the need for Fiscal Policy to address challenges to long-term Economic growth. These were powerful words from Alan Greenspan, who was a powerful Fed Chairman (He established a strong precedent for Fed intervention with the infamous "Greenspan Put".)

Helicopter Hope is the second of two presentations related to Quantitative Easing

(1) Helicopter Money: Analysis of Helicopter Money

(2) Helicopter Hope: Unconventional Play for Unconventional Times

When Alan Greenspan, the former Chairman of the Federal Reserve, states fear that the Economy is at risk of sliding into Stagflation, Americans should take notice. Stagflation is a rare and nasty form of Economic Recession where the Economy is stagnant or stuck in slow growth, while at the same time inflation forces higher interest rates.

The Maestro Chairman Greenspan says "There is only so much that monetary policy can do"

At 3 minutes 20 seconds of the 2nd video clip, Sara Eisen asks Chairman Greenspan about the phenomenon and risk of negative interest rates around the world. Greenspan laments "The whole financial intermediary system is based on Interest Rates received" and then discusses how an extended period of Negative Interest Rates will destroy the Financial System. Greenspan concludes "Monetary policy can only do so much."

Link to CNBC Video Gallery for Segment Two

Quantitative Easing is no longer working

QE has proven unable to deliver Economic Growth above 2%

The Fed recently suggested that buying stocks could help the Economy. This is bad thinking!!!

Let's Change Strategy of QE and Focus on Fixing Student Debt

What is Quantitative Easing and Helicopter Money?

The Federal Reserve has focused

Link to CNBC Video Gallery for Segment Two

Quantitative Easing is no longer working

QE has proven unable to deliver Economic Growth above 2%

The Fed recently suggested that buying stocks could help the Economy. This is bad thinking!!!

Let's Change Strategy of QE and Focus on Fixing Student Debt

What is Quantitative Easing and Helicopter Money?

The Federal Reserve has focused QE on the Asset Side of the Consumer Balance Sheet

QE (formally known as Quantitative Easing) is a Monetary Program where our central bank, the Federal Reserve (also known as The Fed) drives up bond prices in an attempt to increase the Money Supply.

This is a form of Expansionary Monetary Policy. Higher bond prices result in lower interest rates, and lower interest rates are generally viewed to be positive for the the Economy.

QE focuses on the Asset side of the Consumer Balance Sheet. The theory is that asset price inflation creates a wealth effect which inspires Americans to increase spending, which the drives economic growth (consumption is two-thirds of the U.S. Economy).

Since 2008, the Fed has been steadfast in its use of QE. Interest rates in the US have been pushed down near 0%* and record low rates have successfully propped up the stock market. The Dow Jones Industrial Average is 33% above its last peak in 2007.

This was Ben Bernanke's first public speech as a Governor on the Federal Reserve Board. The button below is a line-by-line review of this speech and culminates with Bernanke's case for Helicopter Money. I explain how Helicopter Hope should be adopted.

Helicopter Hope is grounded on the same principles as Helicopter Money

The stock market is at all-time highs

But there is a growing uneasiness that the S&P 500 could falter. Meanwhile, Fed policies have been unable to sustain any Economic Growth above 2%.

This begs the question: Is this the best that QE can do for the Economy?

QE1 saved the Economy in 2008-9. However, the Fed has continued Conventional Quantitative Easing has driven interest rates to 0%, which has hurt Americans with savings (while simultaneously creating "bad inflation" elsewhere). For example, Apartment owners and income property investors have done well, but renters have faced persistent rent increases.

Ben Bernanke made this argument (depicted above) in his Helicopter Money speech.

In addition to the stock market, other investment classes, such as Income Property are also valued at record levels. However, this asset price inflation comes with offsetting "bad inflation" - monthly rent increases have been accelerating. Rapidly rising rental expense puts a real squeeze on disposable income for lower income Americans as well as Millennials.

Since 2009, the average rent in the U.S. Metro area has increased by 25% from $964 per month to $1,200. Recently, labor market data shows that average hourly earnings have been increasing at a rate of approximately 3%. However, wage gains are outpaced the rate by rent increase. Source: REIS Inc and Bloomberg. Reis is a data provider for the Commercial Real Estate industry.

Furthermore, the Fed had destroyed the earning power of Savings through a one-two punch of its Zero-Interest Rate Policy as well as Quantitative Easing

ZIRP has zapped the benefits of savings

Before the Financial Crisis, a retired American would earn $5,000 per year in safe, interest income for every $100,000 in savings. Under the Fed's Zero-Interest Rate Policy, now if you have $100,000 in savings in the bank, the earning power of this same nest egg was slashed by over 90%.

Quantitative Easing is the second hit of the one-two punch against Retired Americans. ZIRP destroyed bank certificates of deposit as a viable savings vehicle. The Fed's massive bond-buying program under QE then proceeded to push down interest rates across all fixed income instruments.

The Fed’s zero-interest-rate policy has eroded interest income, a major concern for seniors and those hoping to live from savings.

Now, the Fed should shift QE to Focus on the Debt Side of the Consumer Balance Sheeet

The primary strategy of Quantitative Easing is to increase asset prices and create a wealth effect to stimulate consumption and drive economic growth.

Yet, in 2016, U.S. Economic Growth has lagged most economic forecasts. In my opinion, the problem is a bifurcated Economy. On the one hand, the 1% is as wealthy as ever as the Financial Markets are at all-time highs. On the other hand, we still have 43 million Americans who depend on Food Stamps.

The Fed has successfully supported the financial markets for years

The Marginal Propensity to Save

Before the Financial Crisis in 2009, roughly half of Americans preferred saving money to spending money. Since the Financial Crisis, the ratio has significantly. Now, more Americans prefer to save money than spent it by a 2 to 1 margin.

The Gallup poll shows a clear trend toward the societal preference for savings. As the U.S. Consumer is Two-Thirds of the Economy, the emphasis on saving money is a slowing force on the Economy.

#HelicopterHope

Optimism Is Inflationary. An Unconventional Play for Unconventional Times

Focus More on the Debt side of the Consumer Balance Sheet

If Debt is the Problem, Fix the Debt

Millions of young Americans are saddled with student loans they cannot repay. (Add to this here)

The Student Borrower Assistance Project warms of aggressive tactics by private loan collectors

Step 1. Refinance All Outstanding Student Debt at the U.S. Government Borrowing Rate, which is currently less than 2% for 10-year bonds. The Fed has Engineered record low interest rates.

The American people own over $1 trillion of student loans through the Federal Student Loan Program. We should tell Congress to pass through the benefits of Quantitative Easing to our student borrowers.

Enter Fiscal Policy

Refinance all outstanding student loans and reduce the monthly payments

Implement Loan Forgiveness and other Negative Amortization mechanisms to reduce Student Loan Debt

Many Americans no longer trust the stock market and it is unlikely they will rush out to spend windfall investment returns. However, helping American reduce debt will is unambiguously positive and more likely to be viewed a permanent improvement in well-being. This is far more likely to create optimism and encourage some spending.

Since 2008, the Federal Reserve Balance Sheet has expanded to over $4 trillion dollars as the Fed has purchased over $1.7 trillion in U.S. Government debt as well as over $1.7 trillion in mortgage-backed securities.

As shown in this chart, U.S. Consumers have never been richer. Net worth bottomed at $54 trillion in Q1 2009 and has since exploded +83% to $89 trillion. From peak to peak, U.S. Consumer Net Worth has increased by 33% from the $67 trillion achieved before the Housing Bubble broke.

Homeownership has strong emotional connection to the American Dream

Excessive monetary accommodation was designed to create asset price inflation. The U.S. Housing market languished for several years. Now the Case-Shiller Index of 20 Cities is within 6% of its matching its previous all-time high set in 2006. Source: Bloomberg

Homeownership Rate Has Fallen Fast. Unintended Consequence of QE, or Something Else?

The U.S. Housing Home Ownership Rate has been falling fast. Ironically, despite steady home price appreciation since 2009, Home Ownership Rate has fallen from the 69% peak achieved in 2004. Source: Bloomberg

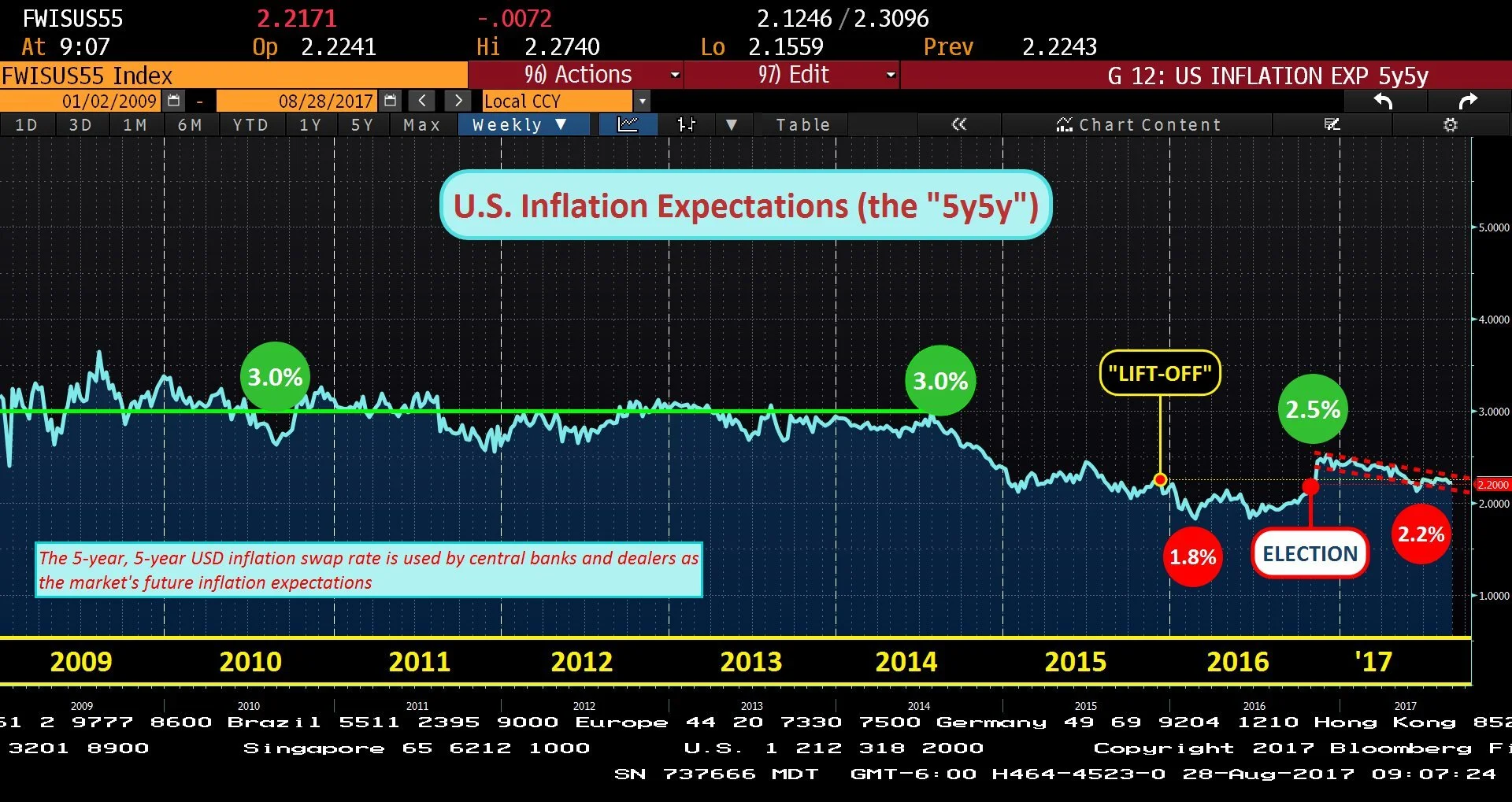

You could call this next chart Wall Street's collective outlook on growth, specifically 5 years out

This is called the "5 Year 5 Year" and it is the markets collective bet on the Projected 5-Year inflation rate, five years from now.

In conclusion, there are two clear deflationary forces in the Economy today

Young Americans: They have too much (expensive) student debt and not enough income. Until they are rightside up, they will continue to restrain their economic participation.

Retirees: Imagine working your entire life to build a nest egg, only to have the Fed eliminate your ability to earn risk-free income on your Savings.

Interest income on savings

(In this environment, we value the certainty of income so high . . . think about the perceived loss of wealth when Retirees can no longer save at a reasonable interest rate)