Winter Update

This Quarterly Update series was first created and published on March 30, 2017 and last updated: December 7, 2017 (In progress & constantly updated, bookmark this link, and check back often)

This Quarterly Update is Part of a Series of Investment Commentaries

The Case For Active Investing | Investing during the Trump Era

Protest Financial Calvinism by Thinking Differently | The Case for Low R-Squared Strategies

Active Construction in a World of Active Investing (Defense Wins Championships)

Quarterly Update | Long Shelf-Life Charts for Investing

In Pursuit of Sortino Ratio via Low R-Squared - The Meridian Equity Income Fund

Financial Rorschachs

This image of Incredible beauty depicts the vast destruction of a Swedish forest

In January 2005, a terrible hurricane-force storm swept through Sweden, felling 75,000,000 cubic meters of forest in its wake. Called Gudrun, this monster was even more destructive than the Derecho that left millions of Americans without power last week. After officials cleared this particular patch of pine trees in southern Sweden, a magnificent pattern of a giant tree emerged. Photographer Joakim Berglund captured the moment in this awesome photograph, which went on to win Sweden’s annual press photography awards in 2006. All these years later, Berglund’s powerful image continues to underscore Mother Nature’s potential for both extraordinary beauty and terror. Prints are available for purchase at the London Natural History Museum. url: https://inhabitat.com/joakim-berglunds-hurricane-tree-captures-natures-beauty-and-terror-in-one-image/

The Big Picture

There is the Asset Economy & the Labor Economy

The Principal Policy Tools are Monetary Policy & Fiscal Policy

S&P 500 is making new All-Time Highs

The Bulls continue to run over the Bears, as the U.S. stock market makes new all-time highs.

Since the $676 low in 2009, the S&P has gained +290% through December 6, 2017.

The Stock market tends to steal the spotlight, but it is the the Bond market that warrants attention.

Depicted below: the 50+year history of U.S. 10-Year Treasury Yield. Interest Rates Have Fallen Steadily over Two Generations (and that's now reversing)

Any Investor under 60 Years Old has known nothing other than the Greatest Bond Bull Market of All Time

The 40-Year Secular Decline In Interest Rates is Ending. From 1962 to 1979, America's insistence on both Guns and Butter (Vietnam and Lyndon Johnson's Great Society) exposed our economic flanks to the Arab Oil Embargo, and two oil shocks culminated in a nasty period of Stagflation. Fed Chairman Paul Volcker earned his spot in history with his decisive victory against inflation. In 1981, the yield on the U.S. 10-Year Bond set its generational high at 16%, and has since declined to 3%. (This chart was last updated on December 7, 2017)

The Greatest Bull Market in Bonds also fueled a massive Bull Market in All Asset Classes

U.S. Household Net Worth & U.S. 10-Year Treasury Yield

Stagflation (1979) USD $8 Trillion with 10-Year around 16%

Cold War (1987) USD $18 Trillion with 10-Year around 10%

Y2K & Internet Bubble (2000) USD $42 Trillion with 10-Year around 6%

Housing Bubble (2007) USD $67 Trillion with 10-Year around 4%

QE Bubble (2017) USD $96 Trillion with 10-Year around 2.3%

Federal Reserve Statistical Release | Z.1 FInancial Accounts of the United States

In 1981, the U.S. 10-Year Treasury hit its generational high yield of 16% as Fed Chairman Paul Volcker tightened U.S. monetary policy to whip inflation. Falling interest rates boost asset prices (in all asset classes: stocks, bonds, real estate, etc.) through the discounting mechanism. By mathematical extension, zero interest rates would act as NOS (nitrous oxide system, a la Fast & the Furious). (The data in this chart was last checked for refresh on December 7, 2017)

The Situation on Wall Street

"Wall Street" is the Asset Economy

The Federal Reserve wants to "Normalize" monetary policy. This means that after 7 years of Zero Interest Rate Policy, aka ZIRP, the Fed intends to gradually increase the Federal Funds Rate.

When the Irrational Exuberance of the Internet Bubble wore off, the Federal Reserve, under Chairman Alan Greenspan cut Fed Funds to 1% to relieve the U.S. Economy of the asset bubble hangover.

While conventional practice, 5 years of this medicine, dripped in steadily increasing doses, allowed another malady to gestate: the U.S. Housing Bubble. So when the Greenspan Fed finally took away the elixir of low interest rates, a swollen Housing Bubble finally bust.

This time, the throbbing of aftermath of the Financial Crisis pounded so hard, that the new Maestro tested unconventional medicine devised only in theory as an application to treat Japan's terminal deflation.

Under Chairman Ben Bernanke, the Fed administered a long and heavy dose of Zero Interest Rate Policy.

The U.S. Federal Funds Rate (also called "Fed Funds") is the interest rate at which Banks lend each other money on an overnight basis. The Fed Funds Rates is set by the Federal Open Markets Committee of the Federal Reserve (the "FOMC") and Fed Funds is a key determinant of the ultimate cost of borrowing for both Companies and Consumers. (This chart was last updated on December 7, 2017)

"Normalization" also means the Fed must Reverse and Unwind QE by Shrinking the Balance Sheet from its All-Time High Level

During the Extended Summer of QE, the Fed injected $5 Billion Per Day into the markets. During Normalization, the Fed will remove $2 Billion Per Day.

Before 2008, the Federal Reserve balance sheet was a Pristine $755 billion, with the securities portfolio invested entirely in U.S. Treasuries. By 2015, the Fed balance sheet increased by 360% to $4.2 Trillion after 3 Rounds of Quantitative Easing. Of the $3.4 Trillion increase, the Fed purchased $1.7 Trillion in Treasuries to keep short term rates low, and another $1.7 Trillion in mortgage-backed securities to stimulate the effect of an interest rate cut below zero. By 2017, the Fed began to communicate its intent to "Normalize" its balance sheet. (This chart was last updated on December 7, 2017)

The $25 Trillion Question with the S&P 500 at an All-Time Highs

Wait . . . No More QE?

The S&P 500 is the most widely followed index for U.S. stocks. (This chart was last updated on December 7, 2017)

Cognitive Dissonance, Illustrated. Despite the Unknown of Reversing QE, the cost of stock market insurance has never been cheaper.

VIX since the Financial Crisis

VIX is the measure of stock market insurance. Unless specified, VIX is usually associated with the S&P 500 Index. (This chart was last updated on December 7, 2017)

VIX since the Internet Bubble

This chart was last updated on December 7, 2017

The Situation, Summarized

The Asset Economy benefited mightily from Low Interest Rates, then got turbocharged by Quantitative Easing.

But Normalization is Coming

Charts updated as of December 7, 2017

The Situation on Main Street

Denver Blue Bear at the Convenstion Center. url: https://www.denver.org/things-to-do/denver-arts-culture/denver-blue-bear-artist/

Scylla & Charybdis

As much good as the Federal Reserve has done, the Fed has also caused misery for many Americans. (Charybdis, the Vortex) Zero Interest Rate Policy, for 7 long years #ZIRP-ed the value of savings while creating dramatic increases in financial assets, such as real estate. (Scylla, the Six-Headed Monster) Asset price inflation in rental property is one factor driving rent to outpace wage gains, causing a Big Squeeze for consumers. It's treacherous out there.

Housing Prices are Approaching All-Time Highs

The Case-Shiller Index hit 206 in June 2006, then plunged during the Housing Crisis and stayed below 140 (a 30% decline) through 2013. (This chart was last updated on October 19, 2017. The data reflects July 31, 2017.) The Case-Shiller home price data is typically cited either as part of a 10- or 20-City Composite. Case-Shiller is the most well known data series cited for trends in U.S. Home Prices. This methodology is designed to track actual observed price changes, and today Standard & Poor's publishes a modified version of this index for 20 metropolitan areas.

Meanwhile, the Home Ownership Rate continues to decline

The Community Reinvestment Act, initially enacted by Congress in 1977 to banish redlining, was revised in 1996.

Finding Affordable Housing is Getting Tougher Each Year, because Rental Vacancy Rates are at Decade Lows

(This chart was last updated on August 18, 2017. The data reflects June 30, 2017.)

Paying Monthly - Apartment Rents

Monthly Rent has been Increasing by over 4%

Since the Financial Crisis, rental property values has increased significantly. This benefits owners of Rental Property, but squeezes Disposable Income for those who rent their housing. From 2011-2016, effective rent has increased by 4.1% annually. (This data set was last updated June 30, 2017)

For Those Earning Hourly - Not Enough Wage Growth

Wage Growth is averaging only 2.5%, lagging Apartment Rent increases of +4.1%

Source: Federal Reserve Bank of Atlanta (This chart was last updated on September 22, 2017)

The Big Consumer Squeeze

The Squeeze, Illustrated. From 2011 to 2016, apartment rents increased by an average of 4.1% and outpaced wage growth of 2.5%.

In this example, Rent has increased from 45.0% to 49.3% of income.

Here is the math to back up the illustration.

"Tight" Job Market and The Consumer

U-3 Overstates Economic Vitality

First Glance, the Labor Market is Tight with only 4.1% Unemployment Rate

The Labor Market is Under-Supplied Hourly Labor

U-3 is the number of unemployment people as a percentage of the labor force (those working or actively looking for a job). (This chart was last updated on December 7, 2017 with data from September 30.)

Second Look, the Labor Force Participation Rate is only 63%

All-Time High Participation of 67% Achieved at the Turn of the Millennium, over a Span of Two Generations encompassing the Invention of Computing, the Sexual Revolution and the Personal Computing Revolution.

Since that Peak, the Labor Force Participation Rate has declined steadily to 63% where it remains stuck. We deduce that as many as 10 million Americans are choosing not to participate in the labor force.

The U.S. working age population (defined 16 to 64 years of age) is approximately 200 million.

Third Point. Current Wage Growth is Not Enough

Source: Federal Reserve Bank of Atlanta (This chart was last updated on December 7, 2017, reflecting data available as of October 31, 2017)

The Consumer Economy

The U.S. Consumer Drives 2/3 of the American Economy

The Conference Board, Consumer Confidence Index

This survey asks respondents to assess current business conditions and appraise their own income prospects. With U.S. GDP growth at 3% and U-3 unemployment at 4.1%, job openings are available, this survey should register strong results.

The Conference Board measures are surging with November 2017 reading 129, the highest scores since Y2K

(This chart was last updated December 7, 2017 using data as of November 30, 2017)

University of Michigan Consumer Sentiment Index

The University of Michigan survey asks respondents to assess current business conditions and appraise their own income prospects. It is important to note that University of Michigan also asks about future buying intentions. Note that the Confidence of Finding Work may not necessarily equal the Intention to Spend Wages.

Michigan continues to hold 98 and looks flattish

Each month, 500 individuals are randomly selected from the contiguous United States (48 states plus the District of Columbia) to participate in the Surveys of Consumers. In order for the results to accurately represent the opinions of the population of the United States, it is important that each person selected participates. The questions asked cover three broad areas of consumer confidence: personal finances, business conditions, and future buying plans. (This chart was last updated December 7, 2017)

Personal Spending

In my opinion, Personal Income growth is insufficient to allow sustainable economic growth

This chart was last updated on December 7, 2017 using data as of October 31, 2017

Personal Saving

This chart was last updated on December 7, 2017 using data as of July 31, 2017

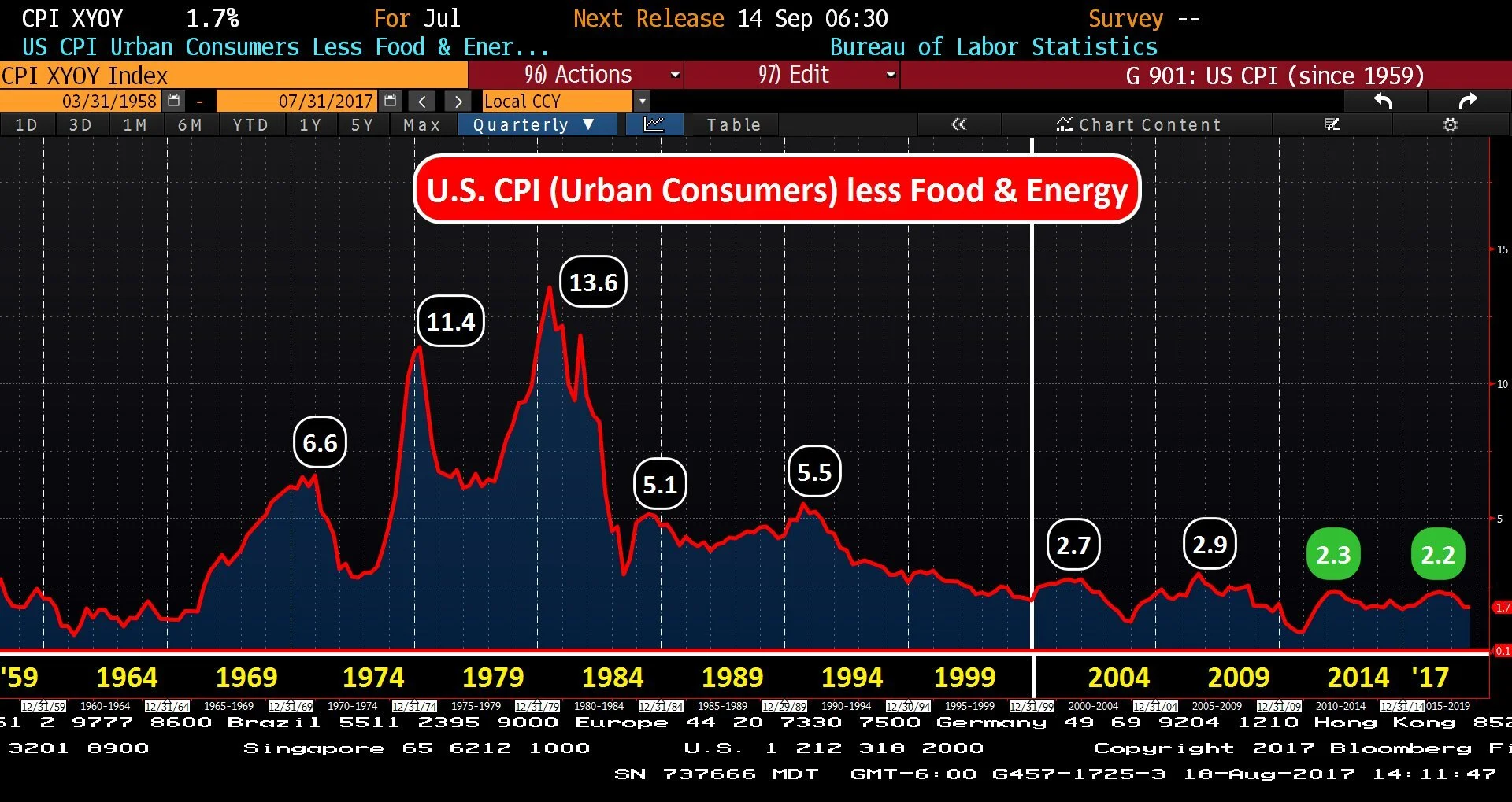

Defying Inflationary Pressures

CPI Has Not Achieved 3% in 20 Years

Reported monthly by the Bureau of Labor Statistics, CPI attempts to measure the change in prices paid by consumers for a market basket of consumer goods and services.

Is 2% Inflation Unbreakable?

CPI remains stuck

Denying Inflationary Pressures

Market Expectations Remain Muted.

The 5-Year, 5-Year (5Y5Y) is the market's guess for the 5-year outlook for inflation, 5 years in the future. This rate also influences the price for U.S. Treasury Bonds.(This chart was last updated on December 7, 2017)

The Trump Factor = 50 bps to the 10-Year Yield

Interest Rates

The U.S. Federal Funds Rate (also called "Fed Funds") is the interest rate at which Banks lend each other money on an overnight basis. The Fed Funds Rates is set by the Federal Open Markets Committee of the Federal Reserve (the "FOMC") and Fed Funds is a key determinant of the ultimate cost of borrowing for both Companies and Consumers.

To calm the Financial Crisis, The Fed and the United States Treasury led rescue efforts. The Treasury provided immediate relief with Bailout capital, to both Wall Street and Detroit. The Federal Reserve responded by implementing Ben Bernanke's Helicopter Money philosophy of the Zero Interest Rate Policy. Under Bernanke, the Fed lowered the Fed Funds rate to 0%. The Fed also purchased nearly $2 trillion of U.S. Government Bonds as well as nearly $2 trillion of Fannie Mae and Freddie Mac mortgage bonds from Wall Street.

Z.I.R.P. The Fed ZIRP-ed the American public to subsidize bank recapitalization. One year and 8 months after "Lift-Off", Fed Funds is 1.16%.

Reflexively, changes in the cost of borrowing simultaneously impact the level of interest income earned by Savers in instruments such as savings accounts and certificates of deposit. American Savers continue to shoulder the cost of recovery from the Financial Crisis as interest rates have languished near 0%.

20-Year History of U.S. Federal Funds Rate: Fed Funds at 5.5% implies an American with $100,000 in savings earned, each year, at least $5,000 in (safe, consistent) interest income. Fed Funds Rate is starting to rise, but #Lift-Off has been under-powered relative to the lost savings income over the past decade.

Alan Greenspan served as Chairman of the Federal Reserve from 1987 to 2006. Greenspan was appointed by President Ronald Reagan and later reappointed by Presidents George H.W. Bush, Bill Clinton, and George W. Bush.

Chairman Ben Bernanke, served two terms as Chairman of the Federal Reserve (from February 1, 2006 to February 3, 2014). He was appointed by President George W. Bush and reappointed by President Obama.

Chair Janet Yellen, has served as Chair of the Federal Reserve since February 3, 2014 since her appointment by President Obama.

The New Incoming Chairman of the Federal Reserve Bank is Jerome Powell.

<3-Month LIBOR>

The London Interbank Offered Rate (LIBOR) is the reference interest rate for trillions of dollars of financial derivative contracts. LIBOR continues to Eek higher each week.

Under Alan Greenspan, 3-month LIBOR declined from 5.5% to a low of 1% in 2003. Coincidentally, and perhaps causally, the U.S. home market started to boom. Interest rates (3-month LIBOR) normalized to 5% by 2006. Then, in 2007, the Housing Bubble began to burst, creating a Financial Crisis and the Great Recession. Fed Chair Ben Bernanke then introduced the Zero Interest Rate Policy, or ZIRP. (This chart was last updated December 7, 2017)

<U.S. 10-Year Treasury Yield>

Depicted above is the U.S. 10-Year Treasury Yield, going back to 2009, the Housing Bubble and the Financial Crisis. (This chart was last updated December 7, 2017)

The Sudden Rise in U.S. 10-Year Yields after Election 2016

(Depicted above is the 1-year chart for the U.S. 10-Year Treasury Yield, last updated December 7, 2017) The sudden rise in 10-year yields after Election 2016. The Election did what the Fed could not - The 10-Year Treasury yield increased by nearly 1% to 2.6%. However, yields have been declining again since the President's 100 Day mark.

U.S. Dollar & FX

The U.S. Dollar Index is the trade-weighted basket of major foreign currencies. The Canadian Dollar is 12% of the Dollar Index. The Japanese Yen makes up another 12%. The remaining ~75% is comprised of the Euro and other European currencies.

(This chart was last updated December 7, 2017) Since 2012, the Dollar Index has surged to 100, but failed to break above this level

<U.S. Dollar Index & 10-Year Treasury Yield>

Since 2015, the Dollar Index (in Red) has poked above "100" several times, but each time, the Dollar has failed to break out above this level.

In Red, the U.S. Dollar Index which peaked at 151 in 1984 and hit another high at 119 in 2001. In white, the U.S. 10-Year Treasury Yield over the same time period.

<U.S. Auto Sales - Another Economic Rorschach>

Auto sales plunged during the Financial Crisis. It took 10 years for US Industry to return to annual sales volume of 17+ million cars. In 2017, car sales slowed significantly to a 16.0 million SAAR . . . until . . .

As of August 31, 2017: U.S. Auto Industry was poised to experience material slowing of new car sales, following a record 18.3 million units in 2016.

September 2017: New Car Sales Estimate bumped up to 18.5 million after Hurricane Harvey impact on U.S. auto fleet

As of September 30, 2017: The sales environment picked up considerably as Americans bought cars to replace those destroyed in the Flooding.

November 2017: Estimate is now 17.4 million

As of November 30, 2017: The Pace of sales slowed from September and October and Auto Sales are now pacing to 17.4 million.

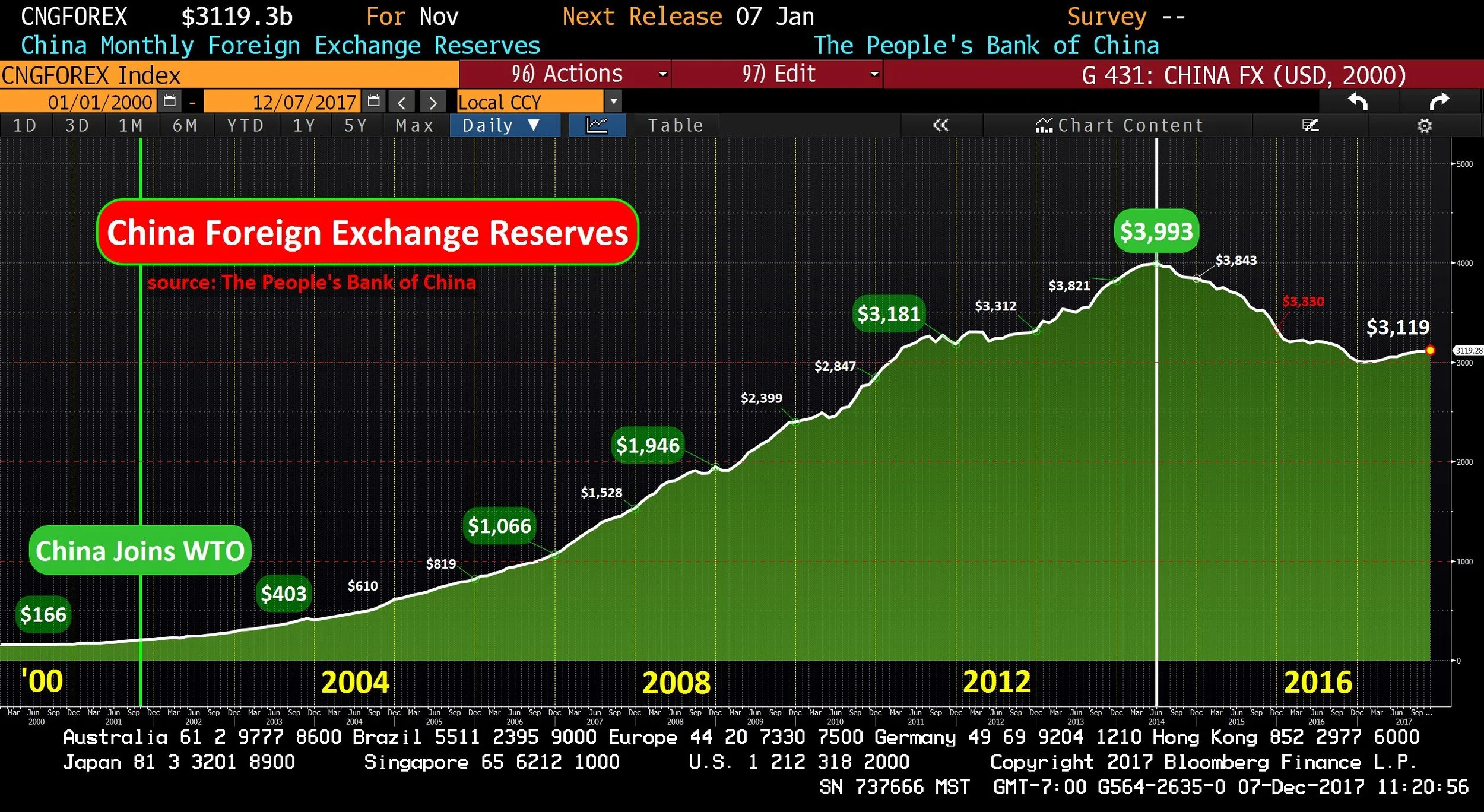

China

<Foreign Exchange Reserves>

Since being admitted into the World Trade Organization in 2001, China accumulated nearly USD 4 Trillion in foreign exchange reserves in less than 15 years

China added USD 3 Trillion to FX Reserves in less than 8 years, from 2007 to 2014

After years of tariff negotiations, China joined the World Trade Organization on December 11, 2001. China pursued an Export led economic growth strategy which led to the accumulation of USD 4 trillion of foreign exchange reserves. In my opinion, this was a 21st form of Mercantilism, which has run its course. (chart last updated December 7, 2017)

China started to hemorrhage cash after 2014. FX reserves have plummeted by USD 1 trillion in two years, 2014 and 2015. (This chart was last updated on December 6, 2017 with data as of November 30, 2017)

<China Oil Demand> This is the most important demand chart for oil, the world's most important commodity.

In 2002, China used approximately 4.9 million barrels per day of crude oil. By 2012, China daily oil demand grew by 5.7 million barrels to 10.6 million - a rate of annual increase of 570,000 per year. From 2014 to 2016 Apparent Demand topped at 10.6 million barrels per day, but has recently broken above this previous high. This data set, available since February 2012, is calculated by Bloomberg under symbol "CHODTTL." (chart last updated December 7, 2017)

Oil

The World's Most Important Commodity

It is about the U.S. Energy Renaissance

Gold

This is a current writing project

The Barbaric Relic